Written on: June 1, 2023 by Phillip J. Baratz

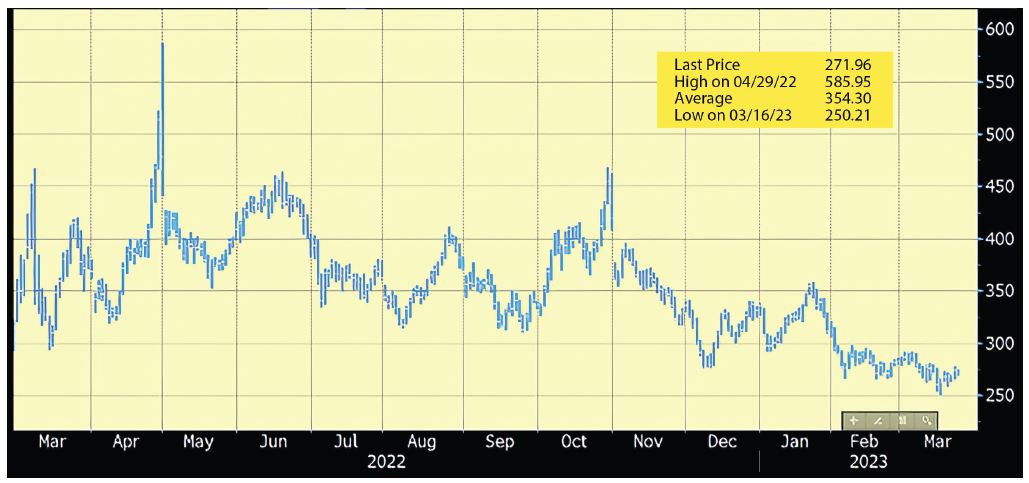

This article is being written in March, almost a year to the day from the first of a series of price spikes that has plagued the world, the U.S. and our industry since Russia attacked Ukraine. Futures prices spiked to almost $4.70/gallon in March 2022. They spiked again to $5.85/gallon in April 2022. In June and then again in October, prices spiked up to over $4.50/gallon (note that we are talking only about the price on the Merc, not the “spot” price in the Harbor or the local rack prices). During that same time period, from March 2022 to March 2023, not only did prices reach highs of almost $6.00/gallon, but they also traded as low as $2.50/gallon (a 240% increase from low to high!).

I do apologize if the prior paragraph gave you flashbacks to last Spring and Summer and the associated sleepless nights as you tried to navigate the extreme price volatility, lack of supply, uncommunicative suppliers and banks, and (mostly) the need to offer comfort to your customers.

Typically speaking, we see pricing programs as among the most certain ways to retain customers (along with service contracts). Within the world of pricing programs, price caps usually do the best job for retention and they continue to grow in popularity. To answer an oft-asked question, “If we don’t offer a cap, is offering a fixed price better than no offer at all?”, I would say that usually the answer to that question is “Yes,” but (as with everything) it is case-specific.

As you learn in Hedging 101, capped and fixed-price offerings need to consider the weather (volume), the price (Merc and basis) and—only in the case of the cap—the “premium” for the protection, usually in the form of a “call” or “put” option (again, case-specific). Generically speaking, the difference between a cap and a fixed price is in the flexibility and the cost. Cap offers are more expensive, but more flexible (prices can’t exceed a certain level, but they can go down—given certain market circumstance, like falling prices). Fixed offers are just that, fixed. They do not have the added cost of the premium for the option on the price of oil, but they also do not have the flexibility to take advantage of falling prices. As the premium for the cap protection is typically passed along to the customer (either as a cap fee or embedded into the delivered price of the cap gallons), dealers got fairly comfortable with the costs and the process. Then came last year’s quandary.

In the Spring and Summer of 2022, caps were very expensive. With spiking prices, record-challenging volatility and extreme basis uncertainty, options prices practically doubled; they often reached levels of more than 50¢ per gallon. The costs to offer a cap became so expensive that some reverted to offering fixed as the “suggested” approach. Ouch.

For example, if a dealer had a choice of offering a fixed price of $5.999/gallon (as insane as that sounded then —and now still!) versus a cap offer of $6.499/gallon, the fixed price might sound more attractive. However, there was a reason for the expensive premium and if/when prices fall more than $2 per gallon, it makes the 50¢ worth of “protection” make a lot more sense. When there is a group of customers paying $5.99, while another group is paying $3.99, some customers in the former group might not be all that happy!

As infuriating as 2022 was to most companies, the ability to capture full margins (and in many, many cases to widen margins) was the result of the extreme price volatility and a far less competitive (dealer versus other dealer) market environment. If you sold product to customers who bought as part of a cap program or to customers who just paid your “street” price, the odds are that on a per-gallon basis, you did very well this past winter. However, the fixed-priced customers did not allow you to increase your margin and many of them felt slighted by being “stuck” with those high prices. When you factor in the warm weather and the extra fixed price gallons that you probably own, fixed price offers were very expensive this year—to the dealers.

Going forward, you need to react, not overreact. You need to hedge, not speculate. Mostly, you need to plan, not guess. The volatility in the market is not something that hardly ever happens. It occurs with regularity and the only thing that we feel is predictable is the unpredictable nature of the business. Consumers want stability—not just your customers, but all customers.

Often, we make things far too complicated, and we don’t have to. If you want to cut down on attrition, offer a program. If you offer a program, offer a cap. If you offer a cap, hedge the risk. If you hedge the risk, consult with a professional so that you will fully understand what you (and your customers) can expect. ICM

PAST RESULTS ARE NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

The risk of loss in trading commodity interests can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. In considering whether to trade or to authorize someone else to trade for you, you should be aware that you could lose all or substantially all of your investment and may be liable for amounts well above your initial investment.