Written on: February 13, 2023 by Phillip J. Baratz

For the past 30 years, companies have been offering pricing programs (fixed and capped) to give their customers peace-of-mind, maximize company sales margins and minimize customer attrition. The methods to offer caps have usually centered around a combination of Merc-related hedges, often locking in “supplier diffs,” and sometimes using physical inventory and/or weather hedges.

The key issue being hedged was generally the price of oil on the Merc, as everything seemed to flow from there. Basis differentials (the spread between the Merc and the price charged by suppliers) were always on the radar, but they were generally stable and were hardly anything that kept people awake at night—the “diffs” did move, but the movements were generally small, just the matter of a few cents per gallon in either direction.

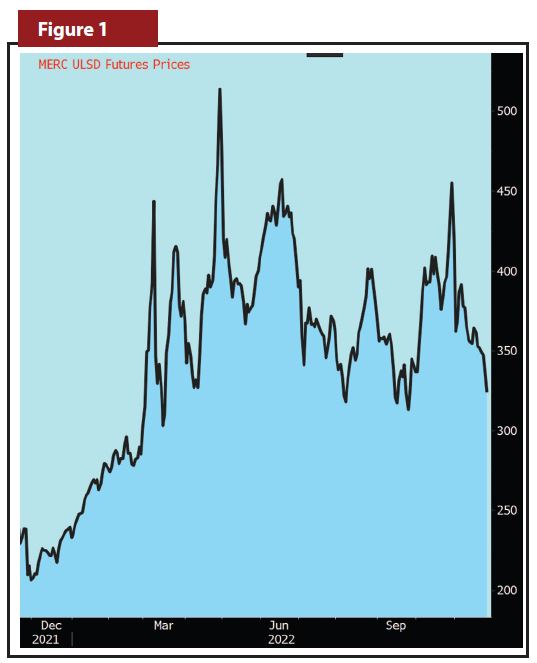

Last February, Russia did the unthinkable and attacked Ukraine. Since that time, the world’s economies have been in flux, the political landscape has become untethered and oil prices have overshadowed all markets (except for cryptocurrencies) in terms of volatility and unpredictability. ULSD futures prices went from a low of $2.00/gallon to a high of almost $6.00/gallon in the late Winter/early Spring—and then fell to $3.00/gallon and rose to $4.70/gallon in the Fall (see Figure 1).

That record-setting volatility drove hedging costs (options premiums) to record highs. Who wants to spend $.50/gallon to cap the price of oil? However, the real issue was not the Merc price or the high cost of Merc-related options. The real issue was something that we had never seen before: a basis blowout so extreme that it restructured all that we know about inventories, futures contract spreads and supplier basis-diffs.

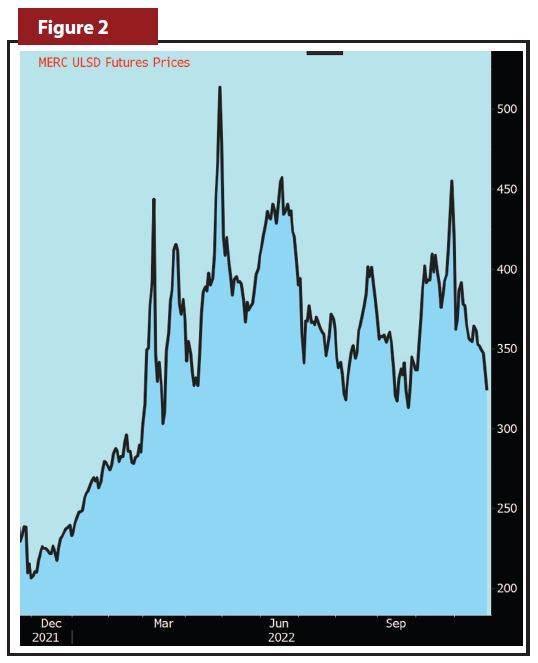

Once the prices spiked last April (see Figure 2), the combination of (a) supply uncertainty and (b) a belief/wish that “all this would soon go away” drove “spot” prices (spot prices, such as those in the New York Harbor physical markets are truer indications of suppliers costs, and accordingly, rack and basis-diff costs) up dramatically and left futures prices at a discount to the spot markets, but not by a few cents. Not by a few dimes, either. The NYH-Merc basis moved out to $1.25 per gallon, well different from the historical average of less than a penny. Ever since the Spring of 2022, we have had futures prices in “backwardation,” where each successive month is less expensive than the one before. In plainest English, it means that physical supply is expected to consistently drop in value over time. That is a recipe for low storage inventories. Who wants to own/hold an asset that is losing value? You need to think deflation as opposed to inflation.

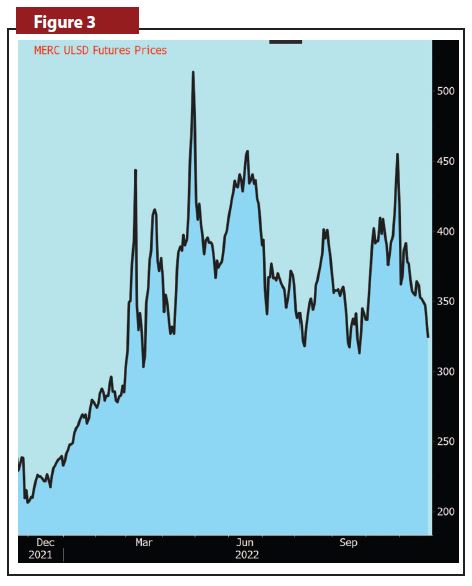

While we had this backwardation over the Summer (see Figure 3), we also had suppliers that were quoting, if at all, seemingly egregiously high basis-diffs for their clients (the heating oil dealers) who wanted to lock in diffs. If there was any good news over the Summer, it was that the basis blowout—spot versus Merc—seemed to have reverted back to its normal boring self.

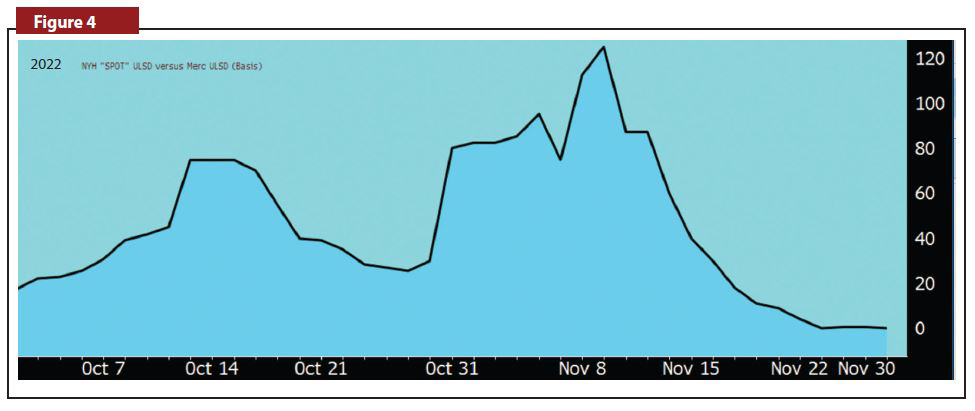

And then October came! In October, the basis spread moved up to about $.75/gallon and then in November it moved up (again) to $1.25/gallon (see Figure 4).

The hope that it was just a one-time occurrence was quickly dispelled. Inventories remained bare, backwardation remained in place and supplier-diffs were still very pricey (note that this article is being written at the beginning of December 2022).

In the future, when the oil market insanity of 2022 is debriefed, there will be a lot of finger-pointing at Moscow and Vladimir Putin. However, a closer look will reveal a lot of other things that have been bubbling up over the past number of years, finally reaching a boiling point—the anti-fossil fuel lobby has led to declining investments in oil production and an absolute curtailment of the building of refineries, all while demand for energy has been increasing. Mixed messages from the U.S. administration about pipeline approvals and the need for more oil production don’t help matters. Worldwide political struggles will always overwhelm the myopic position that the U.S. is a self-sustaining energy producer.

Inventory, suppliers, Greenification, politics, etc. We didn’t start the fire; it was always burning since the world’s been turning. Perhaps we have been lucky that we didn’t have basis blowouts until now.

The three takeaways that we have from this past year are:

1. If you want to keep your customers, you need to protect them from extreme price movements.

2. The larger the swing in prices the more important it is to offer caps rather than fixed prices.

3. Basis protection is no longer a “nice to have” but something that you must have.

You can hedge the basis with supplier diffs (if you can find fair ones), you can hedge with paper hedges (either fixing of capping the basis) or you can pray that 2022 was a total one-off any won’t happen again. What you can’t do is be surprised again. Fool me once, shame on you. Fool me twice, shame on me. ICM

PAST RESULTS ARE NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

The risk of loss in trading commodity interests can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. In considering whether to trade or to authorize someone else to trade for you, you should be aware that you could lose all or substantially all of your investment and may be liable for amounts well above your initial investment.