The saying “customers on a price program are the most loyal” has certainly survived the test of time.

Many of us grew up in this industry that revolved around “churning” customers; while some left each year, they were hopefully replaced by others the following year, and dealers were forced to absorb all the associated costs. The way that many companies accomplished real growth was through a different form of customer acquisition—acquiring other companies.

Although today’s homeowners average the same age as homeowners of a decade ago, their behavior is noticeably different. Homeowners today are tethered to their phones looking for good deals and the latest influencers to tell them what to do. Loyalty has been replaced by “likes.”

As operating costs have increased, the main way to offset those and to still make a reasonable profit has been to increase margins on fuel as well as equipment sales and service. We are fast approaching a collision of dealers who want/need to charge more with customers who want/need to pay less (and are often armed with online information allowing them to do so). Replacement costs for lost customers continue to increase, rendering customer retention that much more important.

Operating a truly efficient business is no longer optimal; it is absolutely required in today’s competitive, information-overloaded marketplace. This means:

• Significant overtime expense in peak months needs to go away.

The good news is that there are tools available to make all this happen right now—with an immediate return on investment (ROI)—not one premised on waiting for customers to hit their third year and have a stable Delivery-K. You need to operate more efficiently, and you need to investigate it now. In addition to the basics of operational efficiency, keeping customers can be as simple as offering them the right pricing program—one that inherently dissuades them from looking for another company while scrolling through social media.

Customers with price caps pay a lower price if retail prices spike, and prices drop if retail prices drop. Free lunch? Certainly not. The cost to provide that flexibility is generally shown in the form of a “premium.”

Given the volatility of ultra-low sulfur diesel (ULSD) futures prices over the past few years—ranging from a pandemic low of 61¢ per gallon in 2020 to a high of $5.13 per gallon in 2022 (an 841% increase) —customers are seeking price protection more than ever. In addition, dealers are seeking customers on price caps more than ever.

How to accomplish this can get a bit complicated. Obviously, you need customers to sign up for the cap, which can be done through existing or new marketing channels including snail mail, email, WhatsApp, bill stuffer, text, auto-dialer, websites, etc. For new enrollments, the message (we have helped many dealers create them) should be simple, straightforward and comforting. For renewals, the communication should include the cap price (the maximum a customer will pay) details.

Hedging can be intimidating, sometimes due to a lack of understanding, the perception that hedging is speculating, or by a preconceived notion/belief of what the markets will do. Does “it won’t go up, the economy is so weak,” or “it can’t drop, there is so much inflation” sound familiar?

Understanding hedging basics:

As mentioned, it is not necessarily easy or intuitive, but there are experts who can walk you through it.

An important note for those offering a pricing program and not protecting against the risk to the profit margin: If you are not hedging, you are speculating.

Track sales/hedges/risk while offering the cap

Your business operating system should allow you to track the “short” side of the price cap (the volumes you have made a promise on). Reporting on this can be done through a business intelligence offering (such as Angus Analytics’ BRITE software), or through an internal report generating system. In addition to tracking the customer (short) side, you need to track the hedged (long) side of the price cap. These positions need to be reviewed on a regular basis, and an overall hedge plan in place determined ahead of time (not based on your gut feeling on a particular day).

While “role playing” of future prices might not be a normal part of your process, it is good to know what will happen if prices make an extreme move higher or lower, or if the weather is vastly different from historical averages.

Points to remember:

• Managing and executing hedge transactions takes a certain amount of expertise and planning and can eventually be mostly on “auto-pilot.”

Don’t let the complications scare you away; we are here to help. ICM

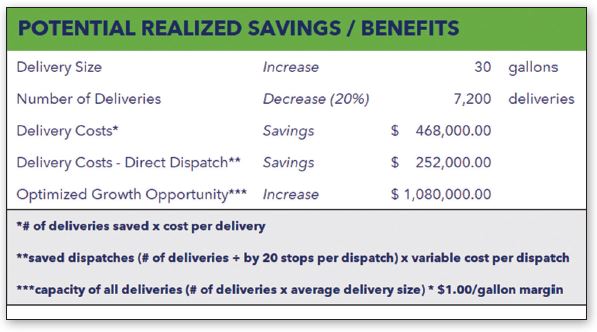

*Please note that there are many details involved in delivery optimization and efficiency and your company will vary somewhat from the industry average. In addition, an increased cost savings is often achievable by shifting around the timing of certain deliveries using AI/ML (artificial intelligence/machine learning) focused on individual data points.

You have data, we have data, and, wow, that’s a lot of data! There is data about trucks and service vans; driver’s wages and dispatcher’s wages; deliveries, stops per hour, miles per stop and costs per stop; costs per delivery, gallons per Heating Degree Day (HDD) and costs per delivered gallon. So much data.

In the realm of residential retail deliveries of fuel, all this data, and the metrics it leads to, are much more similar from one dealer to another than you might think. Yes, driving more miles between stops in a rural area will increase fuel and other delivery costs. However, rural areas typically pay lower wages than urban areas—so these two factors usually offset one another.

With operating costs heading only in one direction (up), unless you can be more efficient, the only way to maintain profits is to increase your margins.

As mentioned, most fuel marketers are within a similar range of efficacy, so many are turning to their pools of data to understand their metrics and then make plans to improve them. Here are some simple points to consider:

Delivering more per truck, which allows you to get trucks off the road, is one of the top goals of some new solutions in the marketplace. These solutions lead to setting achievable goals in coordination with management and dispatch to lower the costs to deliver your product. With a lower cost structure, operators can either run the current business with fewer transactions and moving parts, or (as we have seen in several cases) enabling growth without the necessity of enlarging your fleet or finding new drivers.

However, sometimes there is a disconnect. Helping a dispatcher increase average delivery sizes into 275-gallon heating oil tanks from 150 gallons to 180 gallons is great, and we’ve witnessed this success many times. As exciting as it might be for the dispatcher, and as nice as it is to reduce overtime costs in January, what is the true benefit? What does ownership see?

Ultimately, owners are concerned with the bottom line. In any given year, a host of outside factors can impact the bottom line. Would owners attribute the increase in delivery sizes to an increase in profitability? Perhaps it was a cold winter and consumption was up 10%. Alternatively, if equipment sales slumped because of higher interest rates, the increase of 30 gallons per delivery would be lost in the shuffle. However, the benefits of those increases are imbedded in the company’s profits, but they must be recognized.

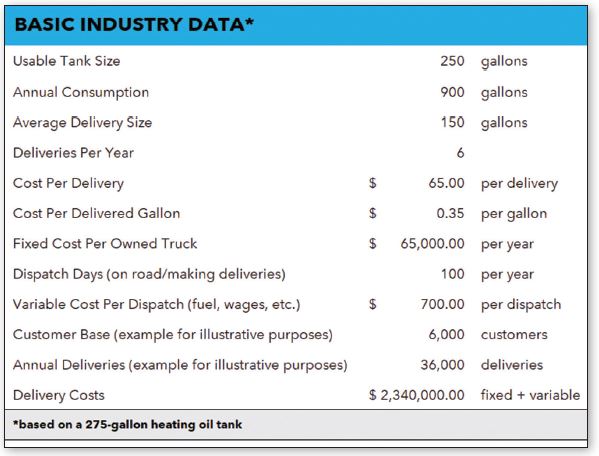

Using “industry averages,” it costs approximately $65 to make a delivery, not including selling, general and administrative expenses (SG&A—which includes the cost of the fleet, fleet maintenance, insurance, wear and tear, dispatchers and driver wages with overtime and benefits)*. If you have 6,000 retail customers averaging 900 gallons of consumption and are averaging 150 gallons per delivery, your “base” is ~36,000 deliveries per year (900 / 150 = 6.

The only thing worse than not enough data is too much data. That can be true while trying to assess the concrete benefits, costs and priorities. Ultimately, at your core, you are a delivery company and if you can improve those costs, you will have a clear and definable set of benefits. The benefits will be in terms of costs per gallon, saved deliveries, gallons per HDD, etc. However, most importantly, they will be clearly defined by extra dollars of profit. ICM

*Please note that there are many details involved in delivery optimization and efficiency and your company will vary somewhat from the industry average. In addition, an increased cost savings is often achievable by shifting around the timing of certain deliveries using AI/ML (artificial intelligence/machine learning) focused on individual data points.

We all know the basic reasons for getting tank monitors:

Regardless of the reason, tank monitors are meant to take away the uncertainty of asking yourself, “How much will I deliver to this tank today?” Better put, tank monitors put an end to the challenge of relying on questionable K-factor consumption calculations. If you know how much you will deliver to a particular tank, you can achieve the two most important improvements imaginable: increased delivery size and optimal fleet management.

You’ve gone out and purchased monitors. Now what?

The decision to buy was likely a combination of economics and emotions. The economics pushed you towards the goals of delivering more efficiently and saving money, while emotion triggered the actual purchase. However, once that decision is made, there is still a lot of work ahead of you. How do you install the monitors? Who installs the monitors? What do you do with the information collected? How do you track value, savings, return on investment (ROI)? How do you know whether your decision was the right one?

We can start with some easy answers. If you don’t install monitors, you will simply have expensive inventory collecting dust on a shelf. If you don’t train your dispatchers and plan how the monitors will improve your results, the investment will not have been worth it. Lastly, if you don’t have an organization that can learn from the data, the purchase was not a good decision.

What should you do?

As with all desired improvements—weight loss, more income, better grades—you need to start with a baseline or a reference point. Do you know your numbers now, before you start with monitors? Knowing your average delivery size is better than not knowing it, but there is a lot more you must know:

Those are some of the questions that you need to ask yourself to successfully plan for the physical deployment (prioritization) of your monitors and the tracking your monitors’ benefits.

If you purchased monitors just to avoid run-outs, it wasn’t worth the investment—you don’t really have that many run-outs. If you purchased monitors just to avoid those frustrating 40-gallon deliveries… well, you don’t have too many of those either. However, if you bought monitors so that you can manage the optimal time to make deliveries for every tank and for every month of the year, then you have the right frame of mind.

Adding monitors without changing your mindset will not achieve your goals. You need to start thinking in terms of days instead of gallons. In addition to considering when a tank has room for a certain sized delivery you must also consider whether that delivery makes sense in the context of the time of year, staffing, overtime and fleet capabilities.

My main point is that monitors are not the solution; they are part of the solution. Monitors are a tool. When coupled with historical data, ongoing reviews and a well-executed operational plan, monitors can (and do) yield fantastic results. We are happy to share some of what we have learned during the past seven years of implementing, tracking and optimizing tank monitor solutions. ICM

PAST RESULTS ARE NOT NECESSARILY INDICATIVE OF FUTURE RESULTS

The risk of loss in trading commodity interests can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. In considering whether to trade or to authorize someone else to trade for you, you should be aware that you could lose all or substantially all of your investment and may be liable for amounts well above your initial investment.

There is an old joke about some guys sitting together talking about their “best” insurance scam escapades that ends with the line, “So, how do you make a flood?” (If you don’t know the joke, you’re likely under age 40!) While it is true that you cannot make a flood, it is also true that we cannot make the weather cold. However, we need to recognize the growing need for our industry to be protected against winters that are not exactly wintery.

The economics of our industry are fairly straightforward: Gross margins are charged per gallon delivered. The number of gallons delivered is based on the number of gallons consumed. The number of gallons consumed (or at least 80% for space-heating customers) is based on the weather. You may not be able to control the weather, but the weather definitely controls you and your profits.

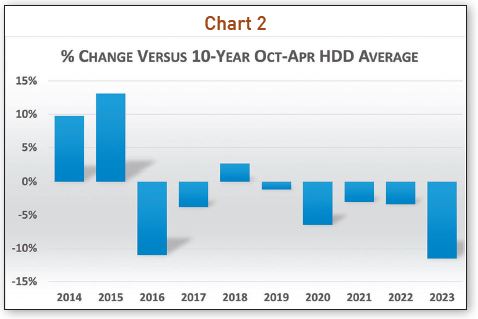

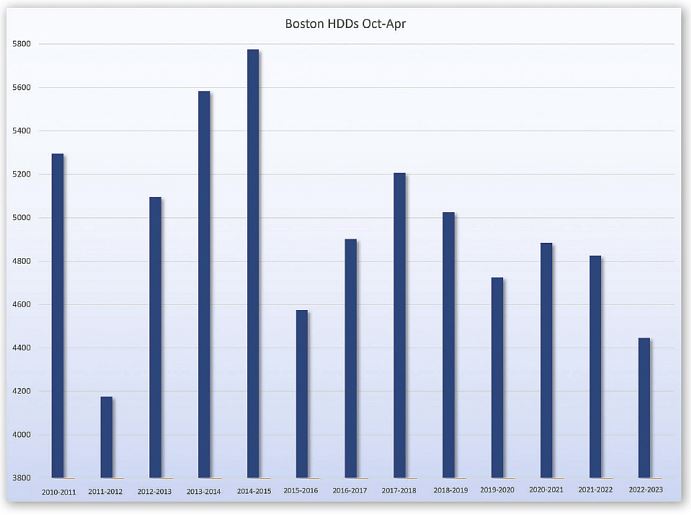

This past winter could have been an absolute financial disaster. Prices were up anywhere from 50% to 150% from the prior year. Interest rates were rising, putting a crimp on all spending, and after a reasonably normal October, the weather in November was warm, and the lost Heating Degree Days (HDDs) never recovered—leaving us with a double-digit percentage loss in HDDs and in sales volumes for heating fuels over the winter.

I said it could have been a disaster, but along with the warm weather in November came moderating prices. Though volumes were light, prices were still relatively high (see Chart 1 for historical ranges over the past five years), allowing per gallon margins to remain strong—in many cases at record highs. If you can manage to sell with record per unit margins, some lost volume might not be that big of a deal. However, if the lost volume were more frequent (see Chart 2 for the weather over the last 10 years, Oct−Apr, at BOS [Boston, MA] weather station), profits would become much less predictable and the operating model would have to change.

The economics in the residential heating fuels industry are mostly fixed—salaries, equipment payments, rent, etc. While there are variable expenses relating to deliveries, you need to keep a fleet of trucks, drivers and dispatchers available to deliver your “normal” number of gallons. It is estimated that to simply break even, sales need to be between 85% and 90% of “normal.” This illustrates why a year that is 1–3% warmer (or colder) might not have a major impact on your bottom line, but once beyond 5%, it can be painful (or, if cold, enjoyable). Further, once we are beyond 10% warmer, we hear about layoffs, deferred capital expenditures, and sometimes uncomfortable conversations with banks and suppliers. In the last eight years, we have had three winters that were 5% warmer and two that were more than 10% warmer.

Prices will vary up and down. Supplier basis will jump about. If you sell your product at rack-plus, these gyrations do not have a major impact on you. If you sell your product—as most do—with the offer of a pricing program, you are familiar with the ways to hedge your offerings to make your per-gallon margins more predictable. You cannot control the weather, but you can control the impact the weather has on your business.

We don’t have opinions on the weather—other than that it is unpredictable. If it is not cold, we won’t make enough money. Risk management (hedging) is exactly that: managing a risk. Your trucks are insured. Your life is insured. Your service techs in someone’s basement are insured. How about your revenue? Is that insured? ICM

PAST RESULTS ARE NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. The risk of loss in trading commodity interests can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. In considering whether to trade or to authorize someone else to trade for you, you should be aware that you could lose all or substantially all of your investment and may be liable for amounts well above your initial investment.

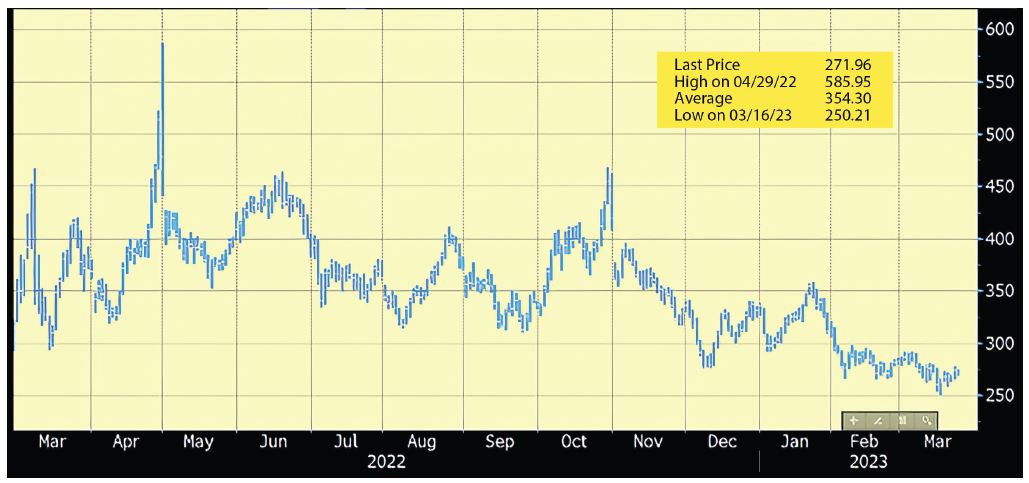

This article is being written in March, almost a year to the day from the first of a series of price spikes that has plagued the world, the U.S. and our industry since Russia attacked Ukraine. Futures prices spiked to almost $4.70/gallon in March 2022. They spiked again to $5.85/gallon in April 2022. In June and then again in October, prices spiked up to over $4.50/gallon (note that we are talking only about the price on the Merc, not the “spot” price in the Harbor or the local rack prices). During that same time period, from March 2022 to March 2023, not only did prices reach highs of almost $6.00/gallon, but they also traded as low as $2.50/gallon (a 240% increase from low to high!).

I do apologize if the prior paragraph gave you flashbacks to last Spring and Summer and the associated sleepless nights as you tried to navigate the extreme price volatility, lack of supply, uncommunicative suppliers and banks, and (mostly) the need to offer comfort to your customers.

Typically speaking, we see pricing programs as among the most certain ways to retain customers (along with service contracts). Within the world of pricing programs, price caps usually do the best job for retention and they continue to grow in popularity. To answer an oft-asked question, “If we don’t offer a cap, is offering a fixed price better than no offer at all?”, I would say that usually the answer to that question is “Yes,” but (as with everything) it is case-specific.

As you learn in Hedging 101, capped and fixed-price offerings need to consider the weather (volume), the price (Merc and basis) and—only in the case of the cap—the “premium” for the protection, usually in the form of a “call” or “put” option (again, case-specific). Generically speaking, the difference between a cap and a fixed price is in the flexibility and the cost. Cap offers are more expensive, but more flexible (prices can’t exceed a certain level, but they can go down—given certain market circumstance, like falling prices). Fixed offers are just that, fixed. They do not have the added cost of the premium for the option on the price of oil, but they also do not have the flexibility to take advantage of falling prices. As the premium for the cap protection is typically passed along to the customer (either as a cap fee or embedded into the delivered price of the cap gallons), dealers got fairly comfortable with the costs and the process. Then came last year’s quandary.

In the Spring and Summer of 2022, caps were very expensive. With spiking prices, record-challenging volatility and extreme basis uncertainty, options prices practically doubled; they often reached levels of more than 50¢ per gallon. The costs to offer a cap became so expensive that some reverted to offering fixed as the “suggested” approach. Ouch.

For example, if a dealer had a choice of offering a fixed price of $5.999/gallon (as insane as that sounded then —and now still!) versus a cap offer of $6.499/gallon, the fixed price might sound more attractive. However, there was a reason for the expensive premium and if/when prices fall more than $2 per gallon, it makes the 50¢ worth of “protection” make a lot more sense. When there is a group of customers paying $5.99, while another group is paying $3.99, some customers in the former group might not be all that happy!

As infuriating as 2022 was to most companies, the ability to capture full margins (and in many, many cases to widen margins) was the result of the extreme price volatility and a far less competitive (dealer versus other dealer) market environment. If you sold product to customers who bought as part of a cap program or to customers who just paid your “street” price, the odds are that on a per-gallon basis, you did very well this past winter. However, the fixed-priced customers did not allow you to increase your margin and many of them felt slighted by being “stuck” with those high prices. When you factor in the warm weather and the extra fixed price gallons that you probably own, fixed price offers were very expensive this year—to the dealers.

Going forward, you need to react, not overreact. You need to hedge, not speculate. Mostly, you need to plan, not guess. The volatility in the market is not something that hardly ever happens. It occurs with regularity and the only thing that we feel is predictable is the unpredictable nature of the business. Consumers want stability—not just your customers, but all customers.

Often, we make things far too complicated, and we don’t have to. If you want to cut down on attrition, offer a program. If you offer a program, offer a cap. If you offer a cap, hedge the risk. If you hedge the risk, consult with a professional so that you will fully understand what you (and your customers) can expect. ICM

PAST RESULTS ARE NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

The risk of loss in trading commodity interests can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. In considering whether to trade or to authorize someone else to trade for you, you should be aware that you could lose all or substantially all of your investment and may be liable for amounts well above your initial investment.

The changes that we have seen over the past several years can no longer be considered an unlucky string of one-time events. The last few years have presented a new set of realities that must be considered for you to continue to build the legacy of your family or your business.

Prior generations were extremely skilled at dealing with the challenges of their day. The current generation is no more or less skilled, but does need to recognize that the challenges of today are different than those of the past.

1. Price volatility: Although we have had our share of extreme movements in the past, such as the Gulf War and the impact of the real estate bubble in 2008, the past few years have made the extreme seem normal. Be it the COVID-19 pandemic, negative interest rates, runaway inflation or the Russian incursion into Ukraine, we have seen a lot of unpredictable price gyration.

a. Flat Price: Simply put, the effect of world events on the actual and perceived demand for oil and the resulting counterbalance attempts by the world’s oil producers.

b. Basis differentials: We have never witnessed both the size and the longevity of the swings we have seen over the past few years, from the pandemic’s negative numbers leading to an extreme dearth of storage, all the way through last year (continuing today) and the heavy carry costs of oil due to the economics of carrying inventory that is worth less as time passes by (negative forward basis).

2. Electrify everything: Rational thinkers worldwide, and certainly those with working knowledge of what it takes to power and heat the people of our planet, recognize that “alternative energies” such as wind and solar power do have niche applications. Those same thinkers understand that, even if it were proven that there was a compelling case to limit or lessen the use of fossil fuels (I would be preaching to the choir if I gave my full thoughts on the subject), it can’t and shouldn’t be done by political fiat in response to activism that does not consider the potential results of their demands.

3. Delivery logistics: Sure, there isn’t much you can do to change the political winds—the bloodlust of some current world leaders or the activism of some famous 20-year-olds—but if there is one thing you know, it is delivery planning and logistics. Prices might go up and down, but your core customer with the K-factor of five will still consume 900 gallons in a normal year with 4,500 HDDs, right? Not any longer. Those Ks have become 5.5s and 6.2s. You need to anticipate and work with those changes.

The world has changed, realities have changed and challenges have changed. Your role is to do what prior generations did: accept the realities, learn from them and adapt to them.

I mentioned earlier that today’s generation is no better skilled than prior generations. That might be true as far as human brainpower, but not true as far as the ability to recognize and adapt much more quickly than prior generations.

We deal with hundreds of companies that serve over two million residential customers. All of our clients are challenged by new realities, and we spend a good amount of time working with them—not to predict the future, but to work with the present.

The new world can be scary. You don’t have to do it on your own. Many professionals can help you with banking, supply sourcing, risk management/hedging, BI (stop “running those reports” and have them automatically done) and delivery efficiency and optimization. Those who will be successful are those who address the challenges head-on. Assess the challenges that apply to you, and don’t be afraid to “phone a friend.” ICM

PAST RESULTS ARE NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

The risk of loss in trading commodity interests can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. In considering whether to trade or to authorize someone else to trade for you, you should be aware that you could lose all or substantially all of your investment and may be liable for amounts well above your initial investment.

For the past 30 years, companies have been offering pricing programs (fixed and capped) to give their customers peace-of-mind, maximize company sales margins and minimize customer attrition. The methods to offer caps have usually centered around a combination of Merc-related hedges, often locking in “supplier diffs,” and sometimes using physical inventory and/or weather hedges.

The key issue being hedged was generally the price of oil on the Merc, as everything seemed to flow from there. Basis differentials (the spread between the Merc and the price charged by suppliers) were always on the radar, but they were generally stable and were hardly anything that kept people awake at night—the “diffs” did move, but the movements were generally small, just the matter of a few cents per gallon in either direction.

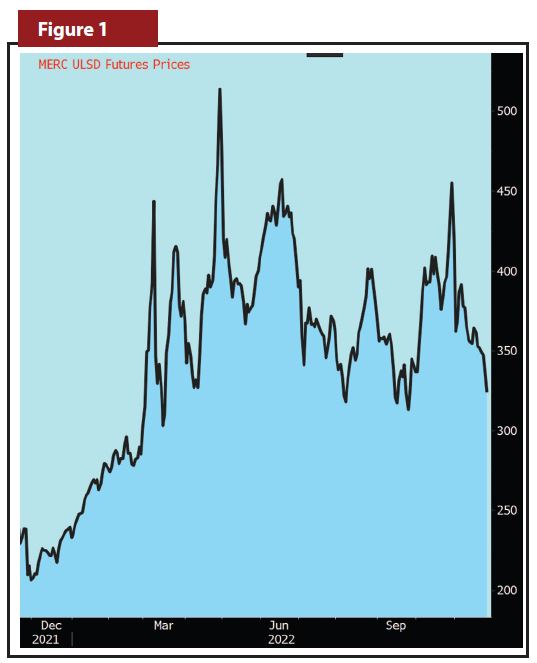

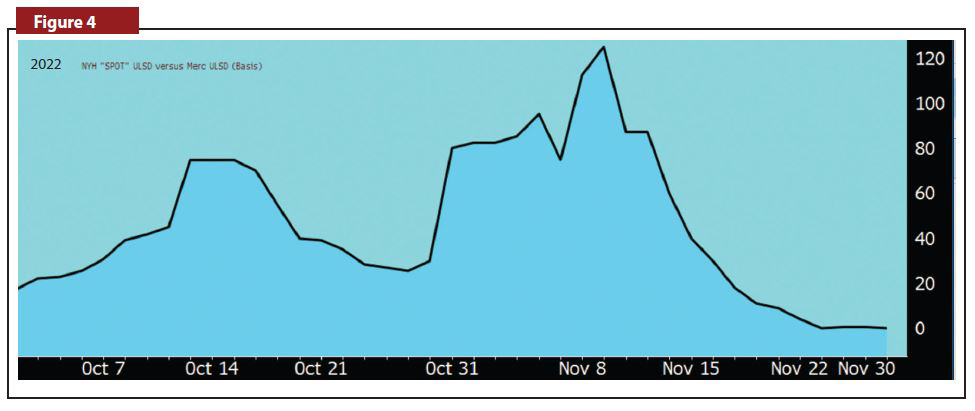

Last February, Russia did the unthinkable and attacked Ukraine. Since that time, the world’s economies have been in flux, the political landscape has become untethered and oil prices have overshadowed all markets (except for cryptocurrencies) in terms of volatility and unpredictability. ULSD futures prices went from a low of $2.00/gallon to a high of almost $6.00/gallon in the late Winter/early Spring—and then fell to $3.00/gallon and rose to $4.70/gallon in the Fall (see Figure 1).

That record-setting volatility drove hedging costs (options premiums) to record highs. Who wants to spend $.50/gallon to cap the price of oil? However, the real issue was not the Merc price or the high cost of Merc-related options. The real issue was something that we had never seen before: a basis blowout so extreme that it restructured all that we know about inventories, futures contract spreads and supplier basis-diffs.

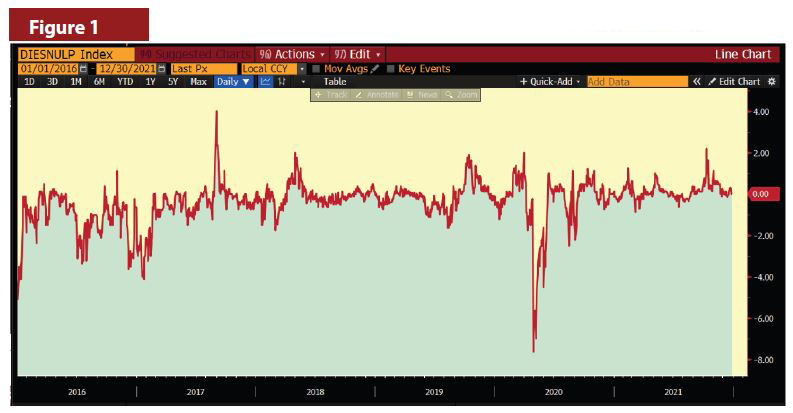

Once the prices spiked last April (see Figure 2), the combination of (a) supply uncertainty and (b) a belief/wish that “all this would soon go away” drove “spot” prices (spot prices, such as those in the New York Harbor physical markets are truer indications of suppliers costs, and accordingly, rack and basis-diff costs) up dramatically and left futures prices at a discount to the spot markets, but not by a few cents. Not by a few dimes, either. The NYH-Merc basis moved out to $1.25 per gallon, well different from the historical average of less than a penny. Ever since the Spring of 2022, we have had futures prices in “backwardation,” where each successive month is less expensive than the one before. In plainest English, it means that physical supply is expected to consistently drop in value over time. That is a recipe for low storage inventories. Who wants to own/hold an asset that is losing value? You need to think deflation as opposed to inflation.

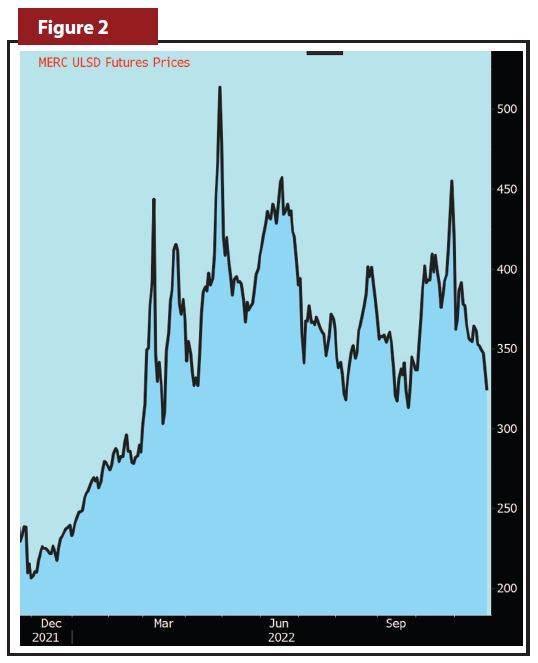

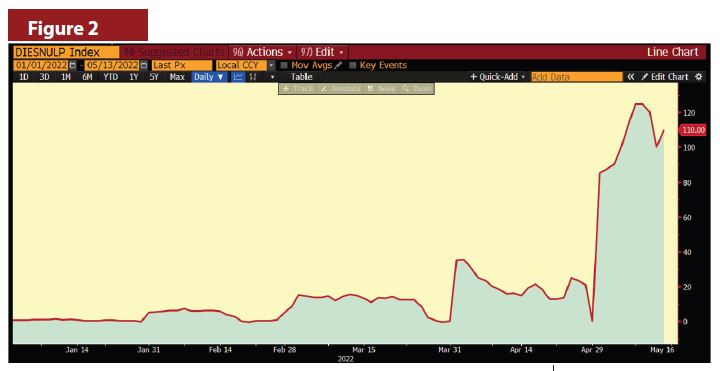

While we had this backwardation over the Summer (see Figure 3), we also had suppliers that were quoting, if at all, seemingly egregiously high basis-diffs for their clients (the heating oil dealers) who wanted to lock in diffs. If there was any good news over the Summer, it was that the basis blowout—spot versus Merc—seemed to have reverted back to its normal boring self.

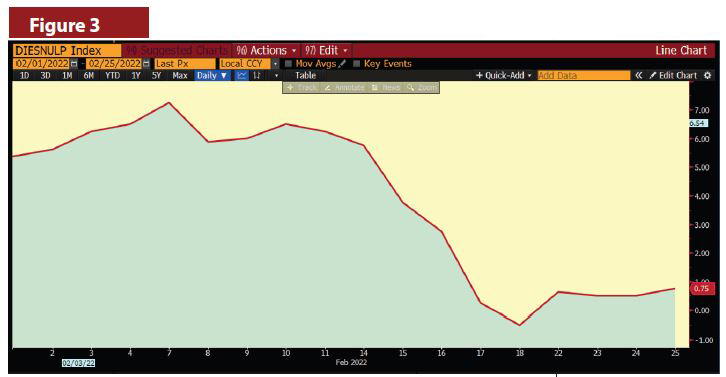

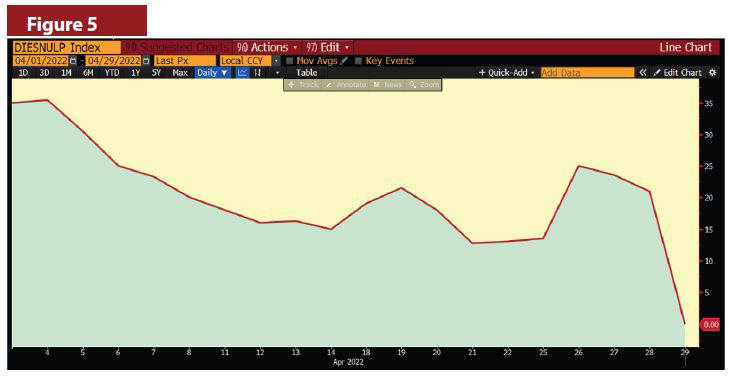

And then October came! In October, the basis spread moved up to about $.75/gallon and then in November it moved up (again) to $1.25/gallon (see Figure 4).

The hope that it was just a one-time occurrence was quickly dispelled. Inventories remained bare, backwardation remained in place and supplier-diffs were still very pricey (note that this article is being written at the beginning of December 2022).

In the future, when the oil market insanity of 2022 is debriefed, there will be a lot of finger-pointing at Moscow and Vladimir Putin. However, a closer look will reveal a lot of other things that have been bubbling up over the past number of years, finally reaching a boiling point—the anti-fossil fuel lobby has led to declining investments in oil production and an absolute curtailment of the building of refineries, all while demand for energy has been increasing. Mixed messages from the U.S. administration about pipeline approvals and the need for more oil production don’t help matters. Worldwide political struggles will always overwhelm the myopic position that the U.S. is a self-sustaining energy producer.

Inventory, suppliers, Greenification, politics, etc. We didn’t start the fire; it was always burning since the world’s been turning. Perhaps we have been lucky that we didn’t have basis blowouts until now.

The three takeaways that we have from this past year are:

1. If you want to keep your customers, you need to protect them from extreme price movements.

2. The larger the swing in prices the more important it is to offer caps rather than fixed prices.

3. Basis protection is no longer a “nice to have” but something that you must have.

You can hedge the basis with supplier diffs (if you can find fair ones), you can hedge with paper hedges (either fixing of capping the basis) or you can pray that 2022 was a total one-off any won’t happen again. What you can’t do is be surprised again. Fool me once, shame on you. Fool me twice, shame on me. ICM

PAST RESULTS ARE NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

The risk of loss in trading commodity interests can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. In considering whether to trade or to authorize someone else to trade for you, you should be aware that you could lose all or substantially all of your investment and may be liable for amounts well above your initial investment.

Savvy fuel dealers have long been aware of the dollar value of a heating degree day to their business. With this realization, many have purchased a weather-hedging product over the years to protect their vital margin in the event materially warmer-than- normal weather could impact a heating season. Most of a typical company’s fuel and service costs are fixed in nature. However, 2022 has introduced a wave of inflationary factors that have driven up these fixed costs, effectively loading up each heating degree day your company will experience this Winter with heightened significance.

In addition to the fuel and equipment supply issues, which have escalated the cost of goods sold just as we approach the peak heating season, expenses associated with payroll, insurance, repair, maintenance and fuel have notably mounted. The borrowing costs associated with tanks, inventory and customer receivables are expected to grow markedly this Winter if the current pricing trend persists.

Many will-call customers may opt to order only the bare minimum needed to make it through the Winter, yet your fixed costs continue. In the span of less than a year, the earnings burden on each heating degree day between November and March has become far more pronounced than at any other time in recent history. With these pressures, it stands to reason that target margins on fuel sales, service and installation can and should be raised, but that “X-factor”—the weather—still looms.

Weather-impacted business

This leads me to the odd question posed at the outset. With each of this coming Winter’s precious heating degree days now stacked higher with the costs of operating your business, have you paused to determine your company’s true required weather-driven earnings?

Fortunately, by using your budget or even last year’s results (if you have opted to navigate these unprecedented times without a forecast), a reliable figure can easily be assessed. While fuel oil and propane deliveries are most obviously impacted by warmer than normal weather, our clients’ experiences show service and installation activities tend to fall as well during periods of material warmth. Therefore, it pays to assess your reliance on each weather-impacted business line.

To many, weather hedging remains a bit of a mystery; however, it is merely a financial tool designed to replace some or all of the lost profitability that would otherwise have been earned in a “normal” heating season. By isolating the most weather-dependent gross profits and comparing them to the expected heating degree days for the same period, a gross profit per heating degree day target can be determined and used to establish protection.

Weather hedges are derivatives and can be structured in a variety of ways and at different protection levels, but the most typical approaches are designed for monthly or seasonal protection. Your commodity trading advisor can assist you in finding the approach that best suits your risk and discussing the costs associated with each approach.

As the recessionary indicators mount, increased bank scrutiny of borrowers’ 2022 financial results is likely to follow. For companies that seek to take advantage of acquisition opportunities, maintaining consistent performance is paramount. Lost heating degree days are shaping up to carry an outsized impact on financial performance this heating season.

Take the time to assess the full weight of what each heating degree day will mean to your company this year. By exploring the tools available to you to help insulate your company during this tumultuous time, you very well could eliminate the need for even heavier decisions next year. ICM

Jeffrey Simpson is the Managing Director of Angus Finance and acts as an advisor to the fuel industry in the areas of hedging, budget preparation, cash flow management, capital structuring, acquisitions, the location of financing and banking negotiations. He can be reached at 860-299-3358 or jsimpson@angusenergy.com.

PAST RESULTS ARE NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. The risk of loss in trading commodity interests can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. In considering whether to trade or to authorize someone else to trade for you, you should be aware that you could lose all or substantially all of your investment and may be liable for amounts well above your initial investment.

Picture this. You sold your customer a capped price of $2.99 per gallon for the winter. Your supplier sells you oil at a price of $2.00 per gallon on a day that the CME pricing (the “Merc”) is $1.90 per gallon. You turn around and sell it for a price of $2.99.

Then a few days later, the Merc is at $1.65 per gallon, but your supplier is still at $2.00 per gallon. You might frown, but you would pay $2.00 and sell it for $2.99. Then a few days later, the Merc is at $1.35 per gallon, but your supplier is still at $2.00 per gallon. You might frown even more, but you would pay $2.00 and sell it for $2.99.

The basis—effectively the spread between the Merc price and your supplier’s price (the “Rack”)—moved, but the customer just paid you your full margin. To a customer, the “basis” means nothing.

Now let’s turn that into the current reality. When dealers offer a price to a customer, capped or fixed, the calculation likely included:

*Merc price (fixed or capped)

*Basis (fixed or floating)

*Profit margin

For the past 10–15 years, the basis has not been a high item on people’s radar. Sure, it was always there, and sure there were ways to hedge it with suppliers or with a trading counterparty, but it was definitely a bit out of sight, out of mind. Companies fell into several categories relative to the basis:

1- Supplier-locked diffs at some point during the summer (with two subcategories)

a. Locked in for most/all of supply

b. Locked in for most/all of the program gallon supply

2- Hedged the basis via “paper” (i.e., a basis swap) leading up to the locking in of the supplier diffs

3- Didn’t hedge or lock the diff because they liked to shop around and didn’t find the basis to be a major concern

Basis versus Merc is somewhat akin to New York Harbor (the “Harbor”) versus Merc. Therefore, according to the “transitive law,” Rack versus Merc is similar to Harbor versus Merc. If there is a blowout in the Harbor versus the Merc, it will lead to a basis blowout at the rack. That is what happened this year, after spending years moving by only a relatively small amount—note the range from

-$.0750/gallon to +$.0400/gallon. Figure 1

Russia then decided that it needed to attack Ukraine and jeopardize the world’s supply balance of oil, causing total disarray and a spike in the “near-term” pricing—and widening of the Harbor to Merc spreads. Note that since January, the spread range (which, over the five prior years was less than $0.12 cents/gallon), is now over $1.25/gallon. Figure 2

The basis blowout has caused program sales gallons to be delivered to customers in May at a net loss to dealers in many cases. Racks have remained somewhat steady with the Harbor, but the blowout between the Harbor and the Merc has led to some serious concerns and sleepless nights as we prepare for this coming year (and years into the future):

1- Will my supplier offer me a fixed-diff for next year?

2- If so, why are they telling me “Not yet?”

3- Also, if so, how high will that diff be?

4- If I haven’t considered locking in a diff, should I?

5- If I should, can I?

6- If I am nervous, is there another approach?

Root cause of blowouts

After studying the movements on the Merc, the Harbor and at the Racks, we believe that we have identified most of the root cause of the blowouts (in addition to suppliers just taking advantage of the situation, and there is nothing wrong with grabbing some extra money when it is available. Heating oil dealers do it all the time!)

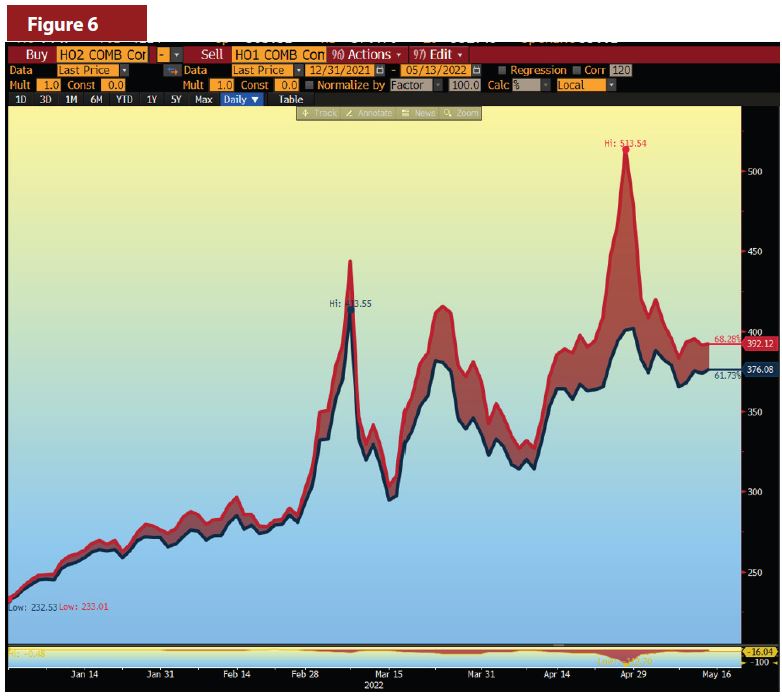

Combining two theories that we both believe are true, we believe a “proxy” exists to curb further basis blowout in the short-term and in total for next Winter. Theory 1 is that, as each month ebbs to a close, the cash market and futures market prices converge. That means that someone owning a futures contract at the end of the month can (technically) accept delivery of that product in the following month. Accordingly, the spread between the Harbor and the Merc tends to narrow down as the month comes to a close (see Figures 3, 4 and 5 focusing on February, March and April and how that diff narrows).

Theory 1 is that since the month ends with the basis pretty close to zero, but we are also seeing some wide Harbor to Merc spreads early in months (painfully so), the pain must be caused elsewhere. Theory 2 is that when the market senses that I need supply now, but in the following month things will be better than today (exactly what we witness in the current “backwardated” market), the spread between two futures contracts will have blown out.

Figure 6 shows how those two contracts (Merc contract 1 and Merc contract 2) track each other and can become totally un-tethered.

A hedge plan may well address the basis blowout through a planned series of spread trades, if appropriate for you. We would assess the volumes that you plan to sell monthly, discuss the amounts that are subject to basis risk (in many cases it might be all gallons), compare the “what ifs” and make a hedging plan for your consideration. Leaving the basis spread as something that doesn’t matter is no longer a viable option.

Remember, customers don’t care about basis, but to you it might mean everything. ICM

PAST RESULTS ARE NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

The risk of loss in trading commodity interests can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. In considering whether to trade or to authorize someone else to trade for you, you should be aware that you could lose all or substantially all of your investment and may be liable for amounts well above your initial investment.