Inside the Mind of Today's Home Heating Oil Customer

Written on: September 23, 2015 by Rich Goldberg

September/October cover story

By Richard Golberg, President, Warm Thoughts Communications

For many years, the oilheat industry has struggled to maintain market share in the face of significant challenges. Not surprisingly, differences of opinion have risen regarding how those in the industry should focus our efforts to fight for our future. Now, for the first time in years, we have substantial, quantifiable data to illuminate a pathway forward.

This spring, six oilheat associations, with funding from the National Oilheat Research Alliance (NORA), joined together to conduct the most comprehensive oilheat consumer study in almost 15 years: The Oilheat Consumer Perceptions and Attitudes Research Study.

Warm Thoughts Communications, Inc. was chosen to conduct the study, which ultimately included responses from almost 2,600 oil customers in Connecticut, Long Island, Maine, Massachusetts, New Jersey and Rhode Island. The results are treasure chests of insights that can help individual companies and industry associations defend their product and customers more effectively.

If you own an oil company, work for one or have a stake in the future of the industry, I encourage you to read carefully and share this with as many people in your company as possible. Some of the findings should absolutely change the way we advertise and the way your employees should be talking with customers when it comes to staying with oil. There is too much data to put in one article, so we will be examining aspects in a series.

If you own an oil company, work for one or have a stake in the future of the industry, I encourage you to read carefully and share this with as many people in your company as possible. Some of the findings should absolutely change the way we advertise and the way your employees should be talking with customers when it comes to staying with oil. There is too much data to put in one article, so we will be examining aspects in a series.

Key Takeaways

There were over 50 questions in the survey, which allowed for substantial slicing and dicing of the data to draw correlations. For example, we asked baseline questions to obtain information such as the age of respondents, gender, number of years in their home, how they bought (e.g. pricing programs, service plans, etc.), location of their tank, whether they had another fuel source in their home or available in their area and more. We then cross tabulated these variables against other factors. We looked at options that included natural gas, propane, electric heat pumps, wood pellets and solar. We even tested some messages that have been used in pro-oil marketing.

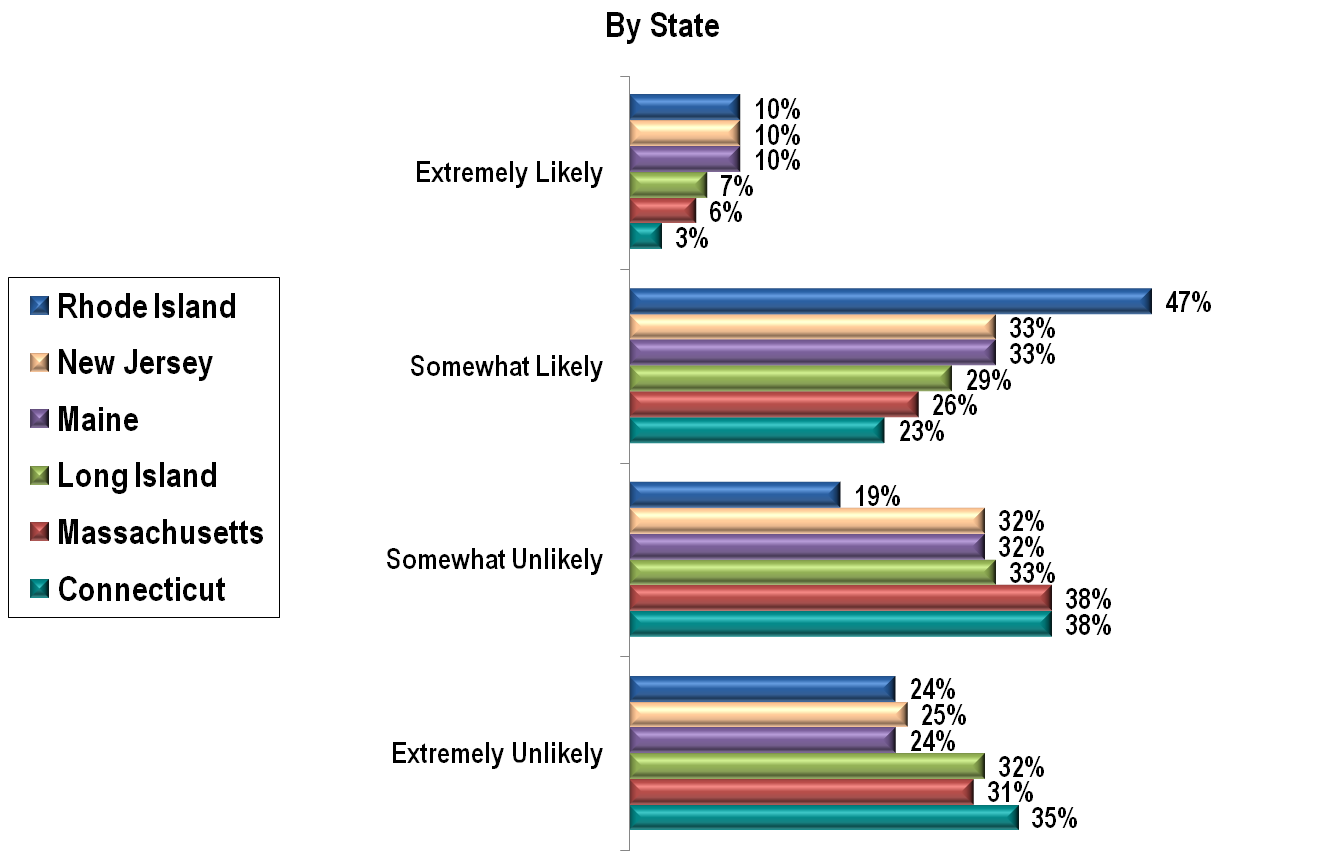

Clearly, we have much to be concerned about, but you knew that already. While the vulnerability to conversion varies significantly from state to state, overall we are in a tough position. That being said, this study provides some reason for hope, and certainly helps clarify the targets and messages that will help our efforts pay off.

Below, I’ve summarized important findings of the summary on a national scale. If you operate in one of the states that sponsored the study, please contact your state association for a more detailed report of the findings in your area. I’ve broken findings into categories of “Bad News” and “Good News” followed by “What Matters” and “What Doesn’t.” First, let’s get the bad news out of the way.

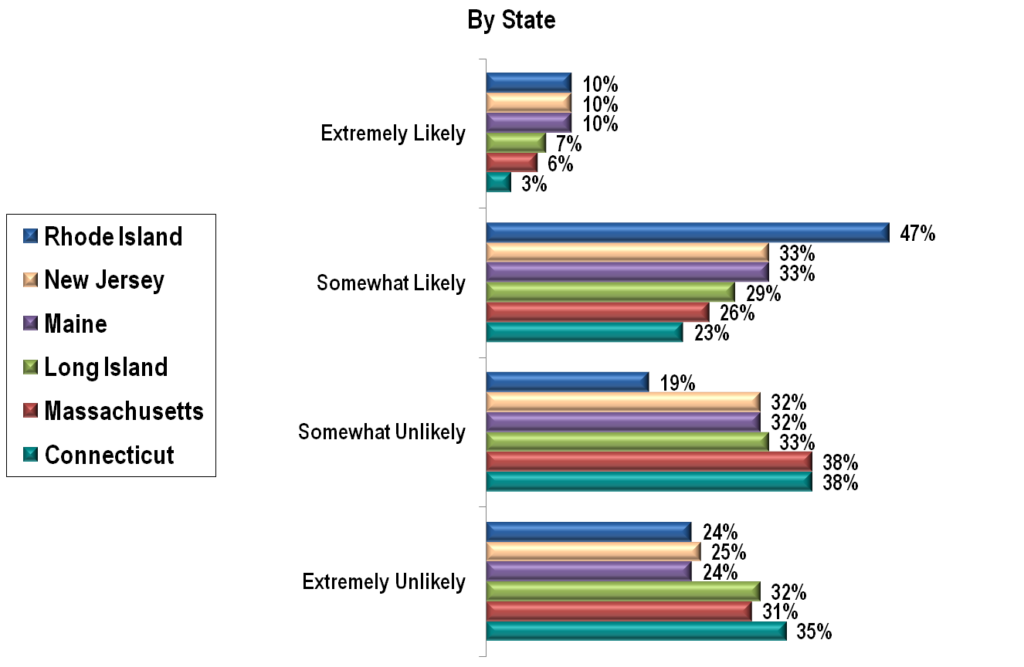

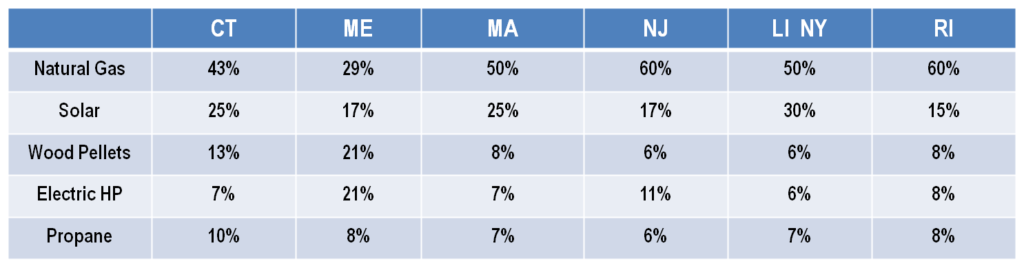

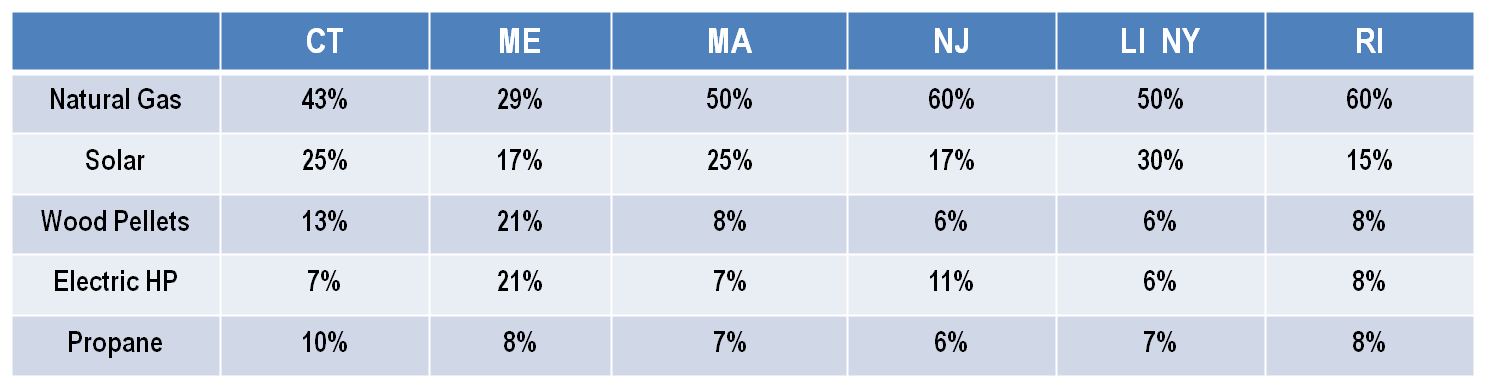

Likelihood to convert, by State (Click all charts for full size)

Bad News

The total number of oil customers looking to convert to another fuel

7% of total respondents say they are extremely likely to convert, and 29% say they are somewhat likely to convert.

The speed at which they wish to convert

Of the consumers who identify themselves as “extremely likely to convert,” three-quarters plan to do so this year or next.

Consumers’ fuel price expectations— perception hasn’t caught up to reality.

41% of all oil customers think their fuel costs will be higher than other options five years from now. Only 6% think heating oil will be less expensive than other fuels.

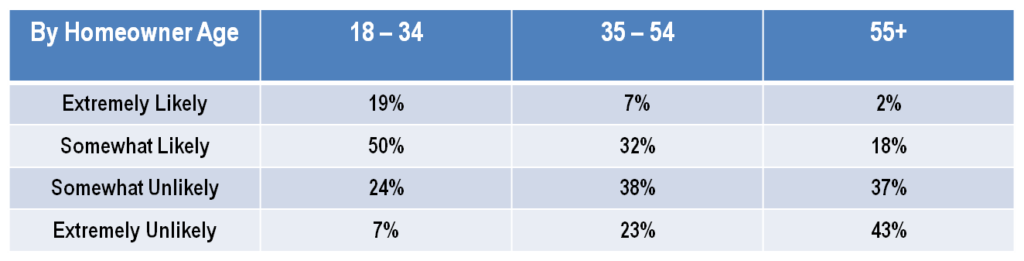

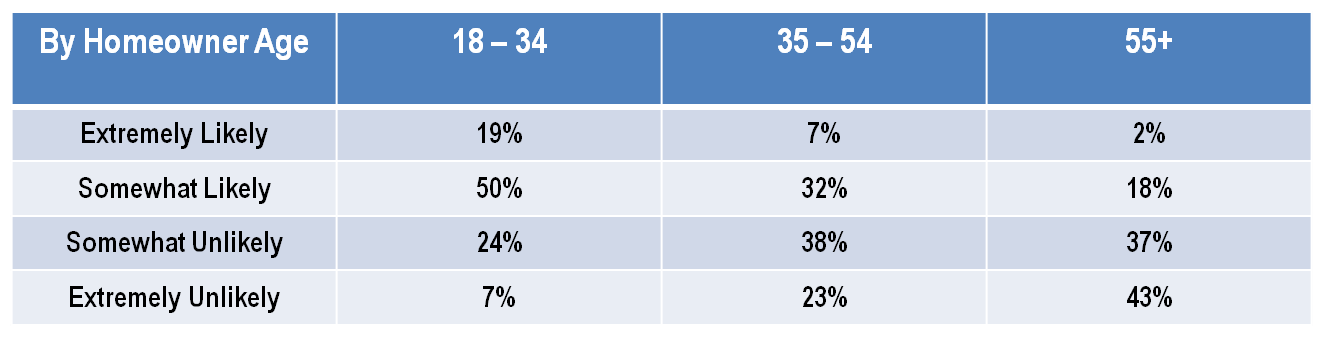

Likelihood to convert, by age

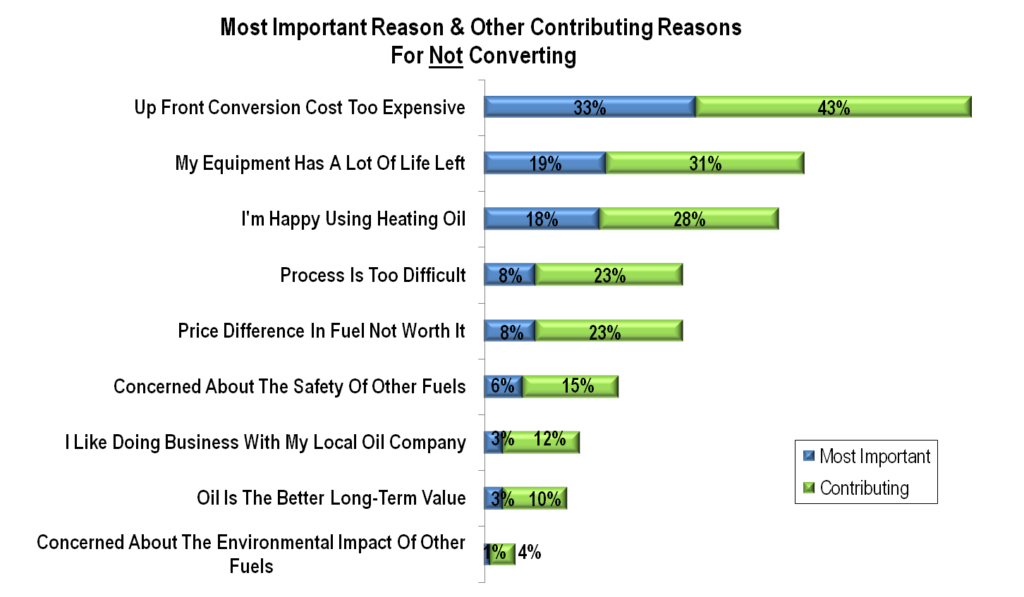

Reasons for not converting aren’t based on strong positives about our product

Of the people who say they want to stay with oil, only 18% say it’s because they are happy using it. The biggest deterrent is actually, “up-front conversion cost is too expensive,” followed by, “my equipment has a lot of life left.” Close behind is, “the process is too difficult.”

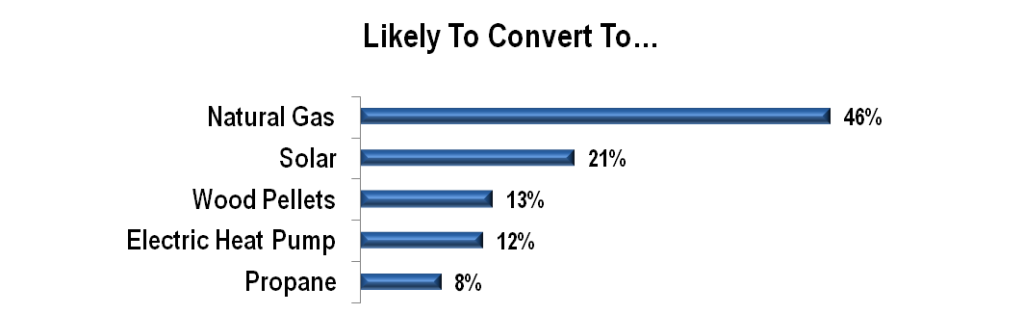

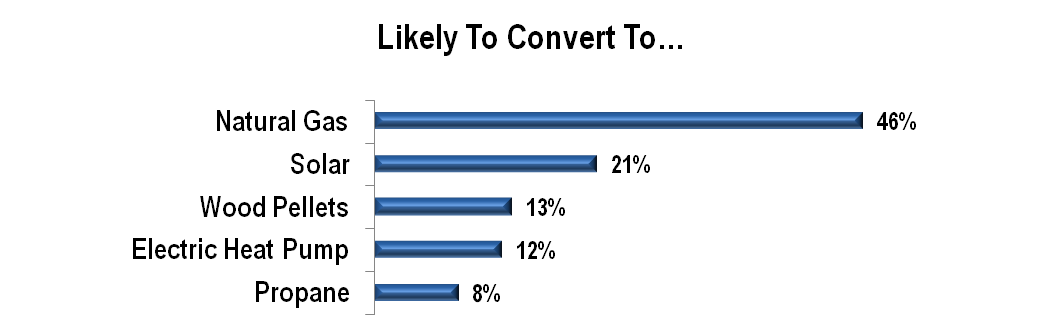

Forms of heating that customers are most likely to convert to

Younger consumers and new homeowners are particularly vulnerable

We are in terrific shape with customers who are 55 and older. Only 2% identify themselves as extremely likely to convert. Unfortunately, that number jumps to 7% in the 35–54 range, and a whopping 19% for those 18–34. Likewise, almost 20% of new homeowners say they are extremely likely to convert. That number drops by a third for those who have been in their homes for one to five years. Unless we figure out a way to make our product more appealing to younger groups, and more attractive to the folks moving into oil heated homes, the future is challenging indeed.

Forms of heating that customers are most likely to convert to, by state

The “extremely likely” group has company

While I have been quoting the number of people who say they are extremely likely to convert, the fact is, two to three times more say they are somewhat likely to convert.

Good News

Their bark is worse than their bite

While 17% of customers have seriously considered converting, only 7% said they were extremely likely to switch. What’s more, 20% of those who plan to convert say they will convert to solar. Forty percent believe it will cost less than $5,000 to convert. So while the interest in converting is greatly troubling, the data suggests that the more customers dig into converting, the more obstacles they’ll find.

Pricing trends were not fully appreciated

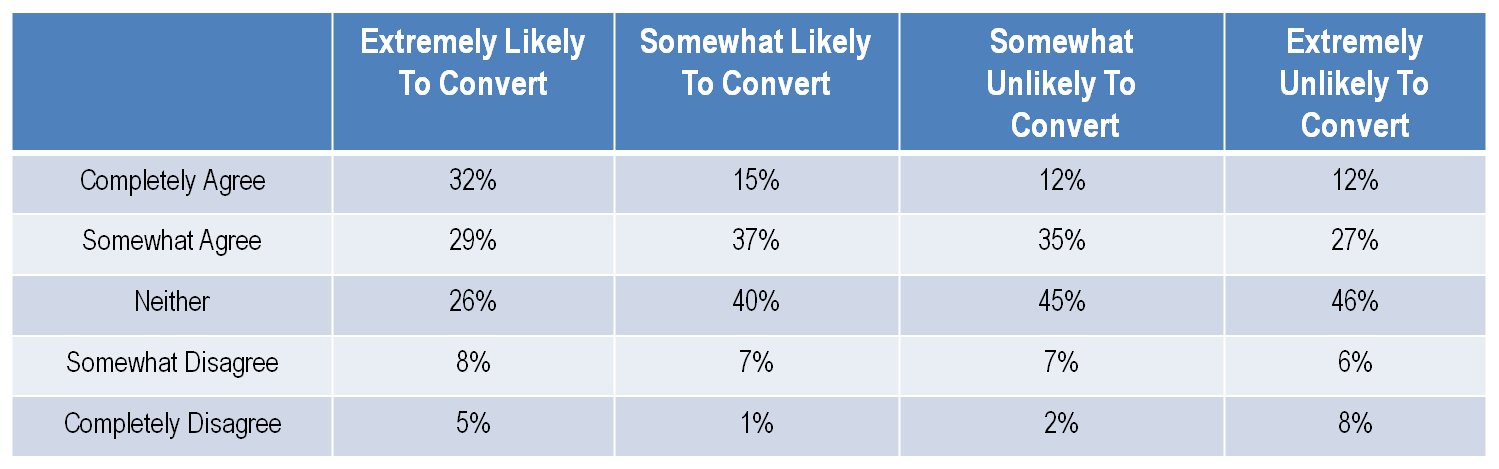

This study was conducted after the price decreases of last winter, which significantly closed the gap with natural gas, and also reduced some of the urgency to convert. However, it seems like consumers will need another year or two of lower oil prices to really rethink their calculations. If that happens, the playing field will certainly shift. But you already knew that, right? Unrealistic expectations about break-even time

Unrealistic expectations about break-even time

Nineteen percent of total customers think that their conversion will pay for itself in less than two years. Forty-six percent think two to five years, and they say they have little tolerance for waiting longer than that. The savings will come almost equally from lower fuel prices and improved efficiency. Those who say they are extremely likely to convert have even higher expectations. Of course, given the current outlook for oil prices and the true cost of conversion, their expectations are even more unrealistic.

Perceived efficiency parity

Generally, oil consumers believe that modern oilheat equipment and can be as efficient as any other equipment in the marketplace, even though we know there is an efficiency gap with the highest gas units. That’s a big deal. Those planning to convert expect that half of the savings will come from improved efficiency. Those efficiency savings could come from a new oil unit, and that hill is not as steep to climb.

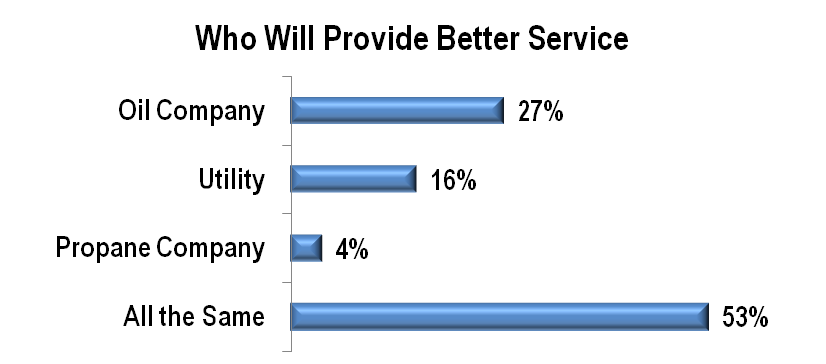

Oil companies are trusted significantly more than utilities

According to the study, when presented with conflicting messages, consumers overwhelmingly place greater trust in their local oil company than they do in their utility company. This gives oil companies a tremendous advantage when taking our pro-oil story to the public.

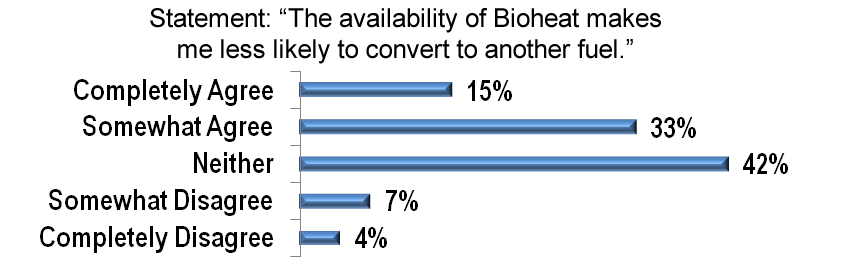

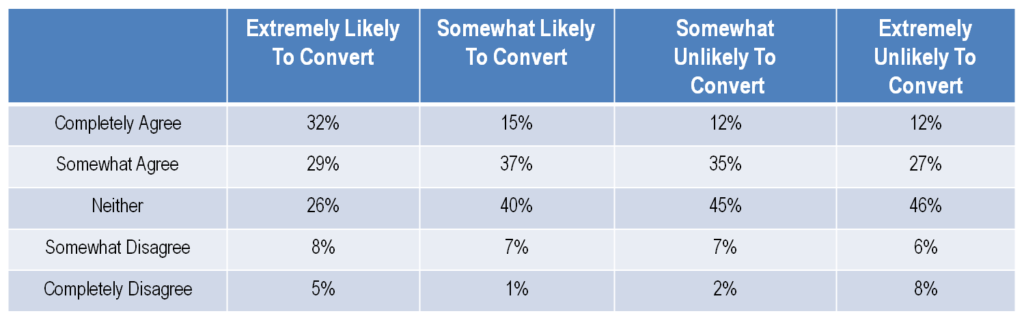

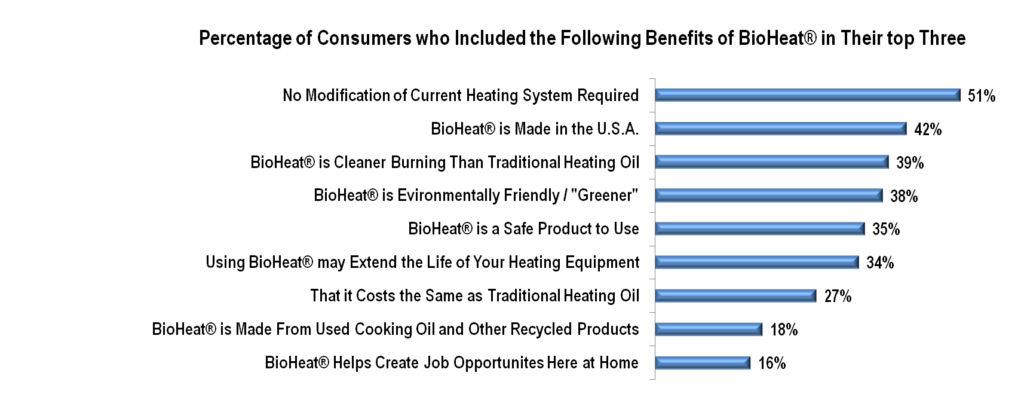

Bioheat is a potential game changer for those thinking about converting

Bioheat is a potential game changer for those thinking about converting

Consumers are looking for an emotional reason to continue using oil and to feel good about it. Bioheat provides that, especially to those who are most likely to convert. Of that group, 64% say that it would make them feel better about using oil, and more than 54% say that the presence of Bioheat makes them less likely to convert. That’s a really big deal. The problem is that less than 12% of oil customers know what Bioheat is.

Implications

Implications

As an industry, we have relatively little money to fight this battle. We need to play smart. We need to focus our efforts where they will do the most good; we need to come up with messages and tactics that will move the needle based on this data.

In our industry, diffusion often trumps focus. This happens in part because of the nature of decision making in associations responsible for administering advertising funds. It is much easier to stuff more angles into an ad or diversify the message to suit important members with different ideas than it is to be disciplined.

Until now, we haven’t had good data on what moves our needle. Now that we do, it will be important to avoid trying to cram our promotions with messages that make us feel good, but that miss the target—hit the outer ring, but miss the bullseye. We simply don’t have enough money or resources.

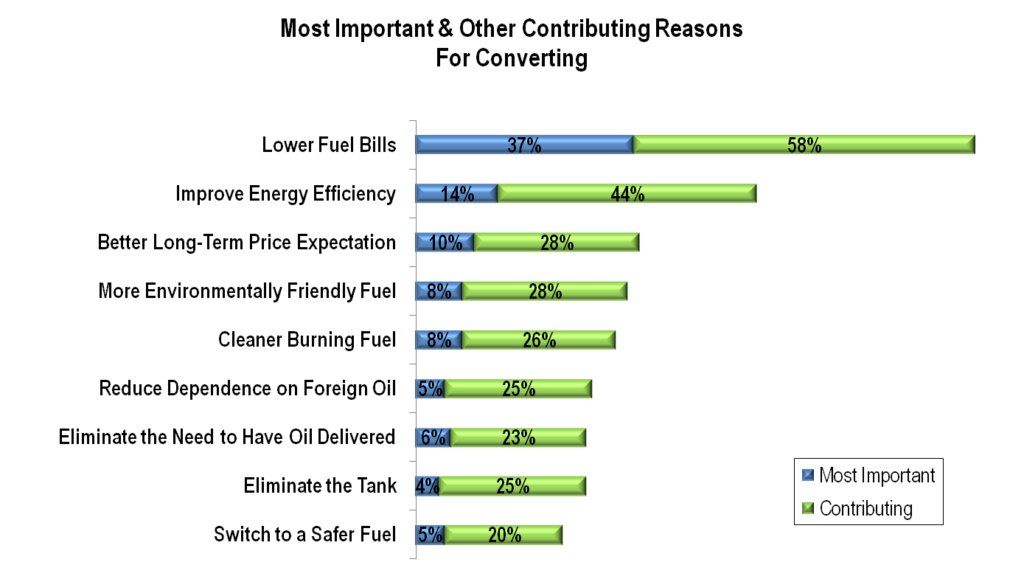

What really matters

What really matters

People rarely make decisions based on just one factor. When we look at reasons people give for wanting to convert, we can combine primary drivers and all secondary considerations so that a fuller picture emerges.

- Lower Fuel bills: Dollars are driving this train. Ninety-four percent of those thinking of converting cite lower fuel bills as a primary or secondary reason. Thirty-eight percent cite better long term price expectation, a related pocketbook issue.

- Energy Efficiency: Improving energy efficiency comes in second, with 14% citing it as the primary driver and 44% citing it as secondary one. Potential converters need to see oil as an efficient option to win their vote.

- Relevant, but not driving the train: After the money issues, all other factors drop off significantly as primary drivers, though several provide strong secondary support. About 25% of customers who plan to convert cite the desire for “a more environmentally friendly fuel” or “cleaner burning fuel” as a secondary influence. A similar number want to “reduce dependence on foreign oil.” These answers help explain why Bioheat connects in a big way, even though it is not a pocketbook issue.

- Bioheat: To customers who are not planning to convert, Bioheat seems to be a nice thing, but not a big deal. To those who are thinking of converting, it is a very big deal, and one of the few factors within our control that can slow down conversions. It enhances the brand and gives those vulnerable customers permission to stay with oil rather than go through the hassle and cost of converting.

- Age of customer: We have the 55 and older vote. If we want to win the election, we need to focus much more on those who are younger.

- Time in home: The data confirms that every time someone moves into an oil-heated home, our risk of losing them goes up dramatically in the first several years. Efforts to focus on property transfers, realtors, etc. appear to be well-grounded.

- Age of equipment: In an interesting paradox, the percentage of customers who said they thought about converting did not vary much with respect to the age of their equipment. In other words, it didn’t matter whether you had a five year-old system or a 15 year-old unit. But when we asked those who weren’t planning to convert to specify why, “My equipment has a lot of life left,” was the number two reason. We suspect it is one of those cases where if they really start looking into it, the younger the equipment, the less likely they are to act on their desire.

- Expected break even: Not surprisingly, the customers who are extremely likely to convert also have expectations of the fastest payback, and voice little tolerance for slower return on investment. Since reality is contradicting that expectation, we win by focusing on this.

- Financing: Roughly half of consumers expect to finance their next heating system purchase. Therefore, having financing options for oil system upgrades is critical.

Joint or individual decision makers: In homes with only one decision maker, there is a bigger inclination to convert away from oil.

What doesn’t really matter

What doesn’t really matter

- How much customers like doing business with a local oil company vs. a utility: The industry does a great job taking care of its customers, and it shows in the very high satisfaction numbers. Only 4% report that they are dissatisfied in any way, but customer satisfaction is not enough to keep them with oil. First, only 27% of respondents believe their oil company provides better service than the local utility. Sixteen percent actually thought the utility would do a better job. The rest called it even. And only 3% identified “doing business with my local oil company” as a primary reason they didn’t plan to convert. Compare that with 33% who cited the up-front cost of conversion as a primary deterrent. The bottom line: even though we want to harp on the virtues of doing business with local, family-owned oil companies vs. the big, bad utilities, there’s very little water in that well.

- Environmental concerns about other fuels (fracking, methane leaks, coal burning power plants, etc.): Consumers are largely unmoved by the environmental issues associated with natural gas or electricity. Only 1% identify it as the reason they plan to stay with oil. We need to leave it alone (though it may have different virtue when lobbying policy makers in government).

- Safety blows: Only 3% say they are staying with oil principally because of safety concerns with other fuels. There are too many homes safely heated with various fuels for this argument to have much sway.

- Buying programs: There seems to be no correlation with pricing programs—cap, fixed or variable—and the inclination to convert.

- Service plans: The same is true of service plans. The study found no difference in the attitudes of customers who had a service plan and those who didn’t. At a recent meeting, this finding triggered a debate. On a practical basis, a big repair bill covered under a service plan eliminates a trigger that could otherwise cause someone to buy a new system, potentially converting in the process. However, that could just as easily be cancelled out by someone who decides now is the year to switch to a different fuel because he’s tired of laying out a lot of money for the plan itself.

- Gender: Whether a customer is a man or woman doesn’t seem to matter much in terms of your inclination to convert.

Summary

This ground breaking study would not have been possible were it not for the executives and boards of the organizations which chose to sponsor it: the Connecticut Energy Marketers Association (CEMA), the Fuel Merchants Association of New Jersey (FMANJ), the Massachusetts Energy Marketers Association (MEMA), the Oil Heat Institute of Rhode Island (OHIRI), the Oil Heat Institute of Long Island (OHILI) and the Main Energy Marketers Association (MEMA), and the support of John Huber at NORA. Many of them spent hours reviewing the draft questionnaire to make sure the results we obtained were authoritative and actionable. It takes vision and wisdom to seek answers that might contradict previous thinking.

The findings we shared above are important highlights, but not the entire story. We will be reporting more information in the coming months. Hopefully, this study starts a dialogue that gets more people doing more of the right things. That will only happen if people know about it, and do something smart with it. That’s where you come in.

If you’d like to obtain a PowerPoint presentation with more of the findings, visit www.warmthoughts.com/norastudy. If you have any questions, you can email me at rgoldberg@warmthoughts.com. You can also post thoughts or questions in the Heating Oil Dealer group on LinkedIn.

The Oilheat industry may be outgunned, but we do not have to be outsmarted.

If you own an oil company, work for one or have a stake in the future of the industry, I encourage you to read carefully and share this with as many people in your company as possible. Some of the findings should absolutely change the way we advertise and the way your employees should be talking with customers when it comes to staying with oil. There is too much data to put in one article, so we will be examining aspects in a series.

If you own an oil company, work for one or have a stake in the future of the industry, I encourage you to read carefully and share this with as many people in your company as possible. Some of the findings should absolutely change the way we advertise and the way your employees should be talking with customers when it comes to staying with oil. There is too much data to put in one article, so we will be examining aspects in a series.

Bioheat is a potential game changer for those thinking about converting

Bioheat is a potential game changer for those thinking about converting Implications

Implications What really matters

What really matters  What doesn’t really matter

What doesn’t really matter