Written on: November 1, 2017 by Phillip J. Baratz

People sometimes get bothered when shown a better way to do things. What those people often infer from the suggestion of improvement is that it is also a condemnation of how they currently do things. Although the title of the article is a bit tongue in cheek, Eight Track tapes were the best way to listen to music. Then, cassette tapes replaced them, followed by CDs and now digital satellite radio. At any point, there was a “best” and the best was good enough for a while, but then there was something better.

People sometimes get bothered when shown a better way to do things. What those people often infer from the suggestion of improvement is that it is also a condemnation of how they currently do things. Although the title of the article is a bit tongue in cheek, Eight Track tapes were the best way to listen to music. Then, cassette tapes replaced them, followed by CDs and now digital satellite radio. At any point, there was a “best” and the best was good enough for a while, but then there was something better.

In our industry, there are many examples of things that were the best at one point in time, only to be replaced (or supplemented) by something even better. Mailed newsletters were great (and for some demographics still are great), but most successful marketers have some digital presence in their marketing plans. K-Factors were an excellent way to make an educated guess as to the amount of fuel in a customer’s tank, but a remote monitor will always be a better way to know what is in a tank—and to make more efficient/profitable deliveries.

The same can be said about hedging for oil dealers. Over the past 20 years, we have seen a good deal of improvement in the way that most dealers hedge their risk, but although many are practicing with the best tools available, perhaps it is time to bridge the gap between “what is” and “what could be” with regards to managing risk.

The notion of hedging is still the same as it has always been: to transfer the risk that you have, related to the sale of oil to your customers, to someone else willing to assume that risk. Transferring the risk, generally the price risk, allows dealers to more efficiently compete and grow by controlling margins for fixed and capped offers, as well as managing the cost of inventory in storage or wetbarrels to be purchased at a time in the future.

Although contracts are generally in full 42,000 gallon (1,000 barrel) increments, there are ways to customize hedges down to the actual needed volume. Today, and for the last number of years, you can match your price risk (in the case of a cap, your risk might be that prices would increase, raising your cost of oil and cutting into, or eliminating, your profit margin) against the volume that you plan to sell each day/month/season. It sounds like a pretty envious position to be in for a dealer—transferring both price risk and volume risk. It actually has been a “best practice” for a while, but we have been wondering if this is all that can be done.

In a typical example, a dealer might assume that he or she will sell 22% of their annual volume in the month of January. That assumption is based upon historical heating degree-days, and the specific delivery history to the customer base. On average, indeed, 22% of the volume is delivered in the month of January. However, it is rarely exactly 22% of the delivered volume! Sure, January is a cold winter month, but sometimes it is only a little cold (say 20% warmer than an average January—like we have seen a couple of times lately), and sometimes it can be much colder—say, 20% colder than average. In actuality, it is rarely average—and that led us to realize that “average” and “normal” are not the same thing.

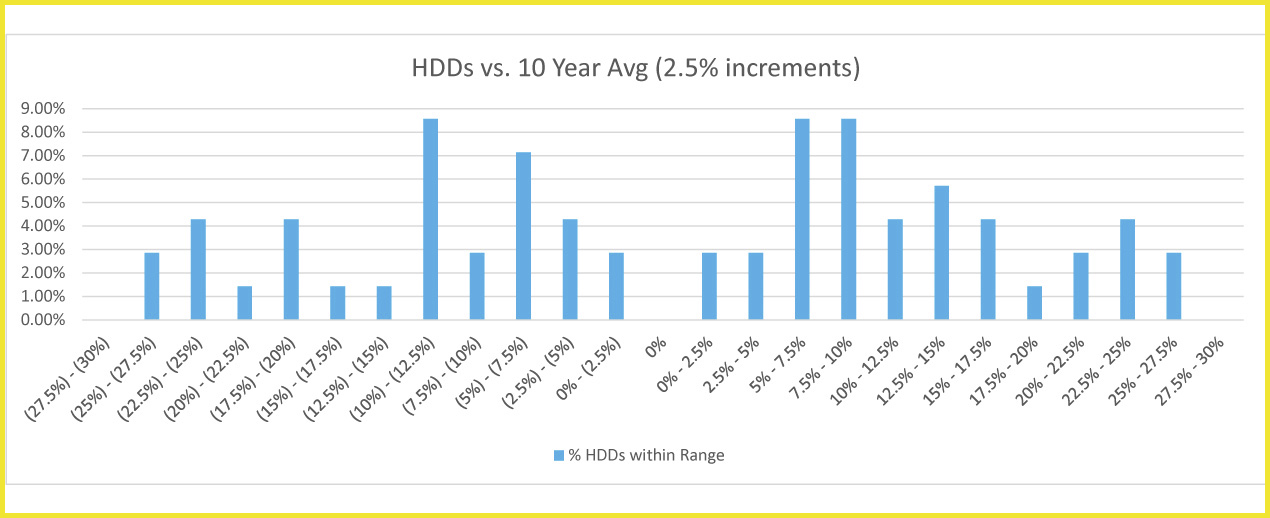

This chart shows the distribution of actual Heating Degree-days (HDD) as compared with the 10-year average for each month over the past 10 years (70 data points = seven months times 10 years). As you can see, the actual monthly HDDs are all over the place, with very few actually close to the average.

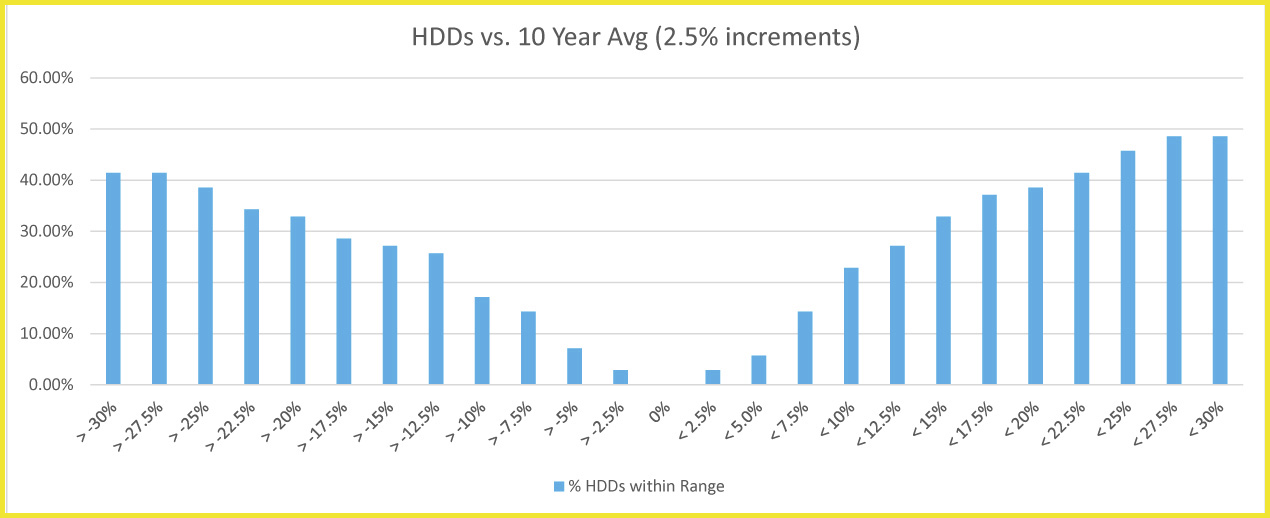

This chart shows how wide you need to go to truly capture what would be deemed to be “normal.” As you can see, 80% of months are between 80% and 120% of average, whereas 88% of months are more than 5% higher or 5% lower than the average. In other words, hedging with “average” volume is almost always going to leave you with either not enough gallons hedged or too many gallons hedged.

When you don’t have enough gallons hedged (due to cold weather), and prices rise (as there is a good correlation between weather and price), you are likely buying those needed gallons at a rising price.* On the other hand, if it is warm and you are “over hedged,” those gallons are more than likely at a falling price* and you will have to sell them into the marketplace.

We feel that it is time that dealers look to limit the volumetric exposure that is inherent, and, as the charts show, are very regular. By looking to further customize either swaps or options to match not only the price risk (strike price or swap/futures price), but also matching the volume with that actual weather—not the historical average weather—another layer of uncertainty can be transferred (hedged) to a trading partner who is willing to assume that risk.

Think about the months when it got cold and you simply didn’t have enough hedged gallons to match your delivery obligations. Or, perhaps even worse, what about the warm months that leave you sitting with gallons that not only don’t you have a need for, but you also have financial exposure—such as with a fixed price offering or with gallons in storage.

There is not enough space (and, I prefer that my readers don’t fall asleep) to go into the details of how to better hedge volume in addition to price, but the complexities are not that great, and the cost benefits might be enough to make you wonder why this article hadn’t been written before. Settling your trades against a predetermined volume is a very good way to hedge, and given the way that the industry moves, it may be considered a very appropriate way to do so. Settling your trades against something—the actual weather— that more closely matches up against your deliveries may soon become the best practice.

PAST RESULTS ARE NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. The risk of loss in trading commodity interests can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. In considering whether to trade or to authorize someone else to trade for you, you should be aware that you could lose all or substantially all of your investment and may be liable for amounts well above your initial investment.

*Please note that we are not opining on whether the weather and price will follow each other. They might and they might not. There are strong historical correlations, but our main purpose with this type of trade is simply to match risk volumes with hedged volumes.